How to write a corporate sustainability report?

Corporate Sustainability Reports (CSR) are the information disclosures that companies respond to the issues concerned by stakeholders and fulfills its responsibilities, and implements the concept of sustainable management for the company, so as to demonstrate the commitment, performance and results of social responsibility, environmental protection and sustainable management. Environmental, Social, and Governance (ESG) proposes the principles of how to practice CSR, and evaluates the sustainable development indicators of enterprises from the perspective of environment, social and governance.

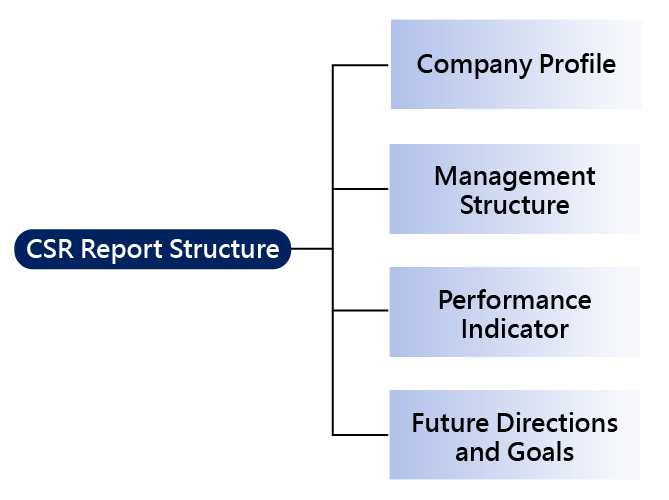

The report, Corporate Social Responsibility Report and Corporate Sustainability Report alike, is a tool for an enterprise to communicate with its stakeholders, and it puts into consideration the corporation's operation in economic, environmental, social and cultural aspects to enable long-term corporate development by formulating strategies and through employee development in a transparent and proper manner. Appropriate contents report should fully and transparently disclose information.

- The framework, policy, and action plans for the implementation of the corporate social responsibility.

- Major stakeholders, topics of their concern and the boundaries of the topics.

- Results of performance and reviews of the corporation's implementation of company governance, development of sustainable environment and the maintenance of social welfare.

- Directions, goals and management approaches for the future.

1. Select guidelines for disclosure reference

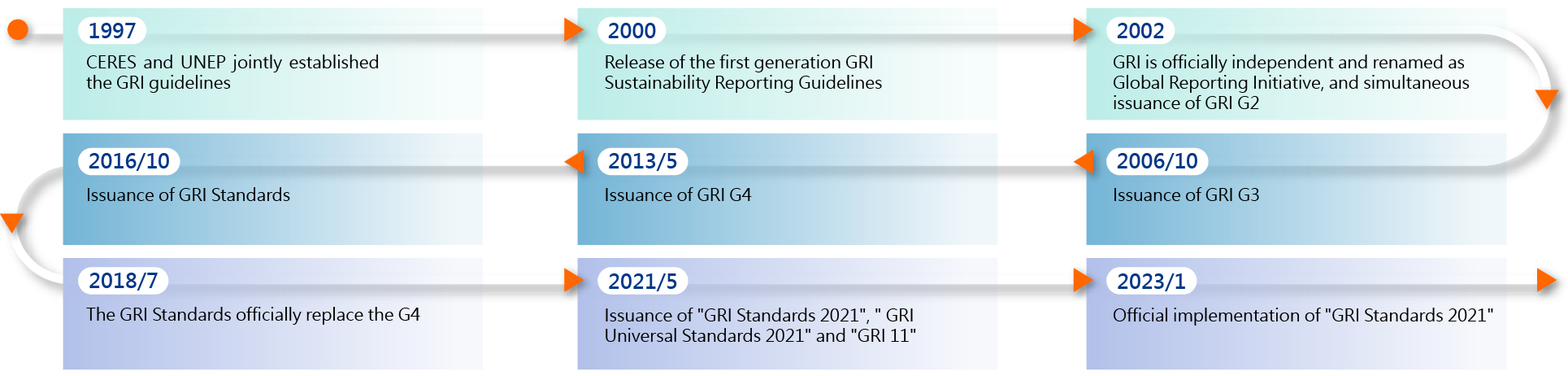

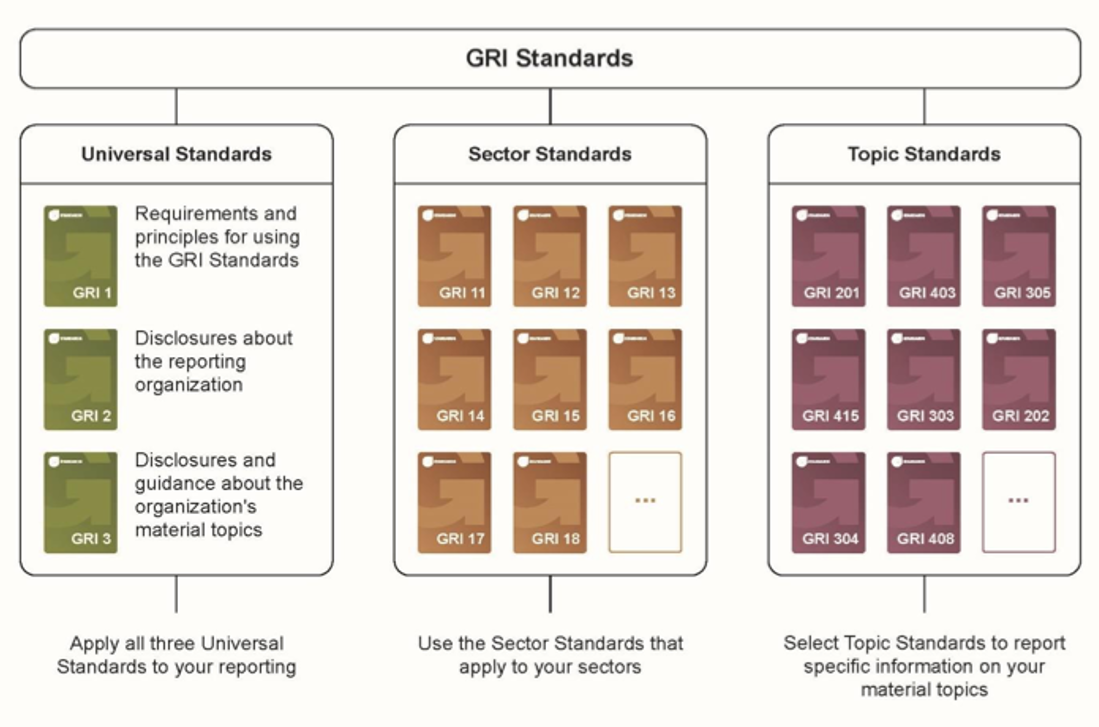

There are fixed guidelines for the content and structure of sustainability reports for reference. The GRI Standards established by Global Reporting Initiative (GRI) is currently the most widely used global standard for corporate sustainability reporting. The content of corporate reports must at least include information on the nature of the organization, material themes, and related shocks and how to manage them.

In 2021, GRI will release a new General Universal Standard 2021, which compared to GRI Standards, enhances the disclosure of information related to an organization's operations and the progress of an organization's transition to a low-carbon economy. The key points of this revision include the adjustment of the number and name, the revision of the Management Approach to the Material Topics, and the revision of the reporting principle to integrate the content of the current report with the quality principle, and the addition of sector standards guidelines to provide recommended disclosure standards.

2. Identification and communication of stakeholders

Stakeholders refer to entities or individuals that are impacted by the corporate activities, products or services, and whose actions would also affect the company's strategies or ability to achieve goals.

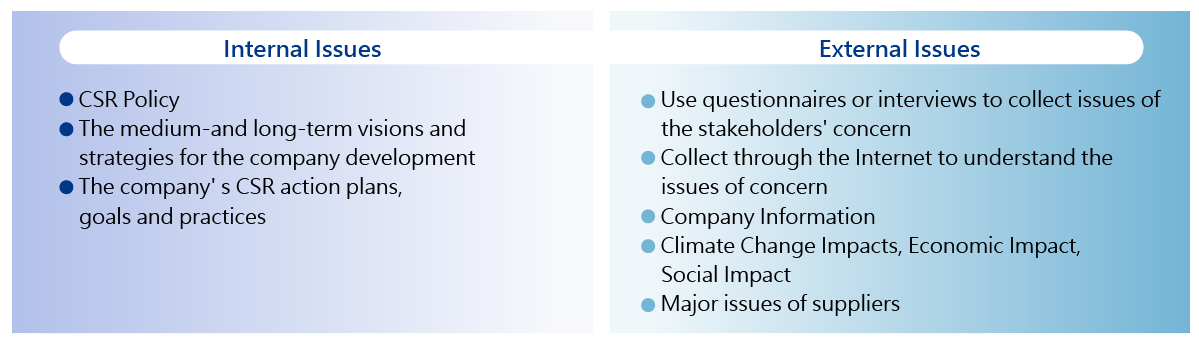

Establish a complete list of stakeholders, then summarize the categories of stakeholders, evaluate their importance, and identify the most important stakeholders in the company's communication, and communicate through questionnaires, interviews, shareholder meetings, seminars or supplier audits, etc. Master its concerns.

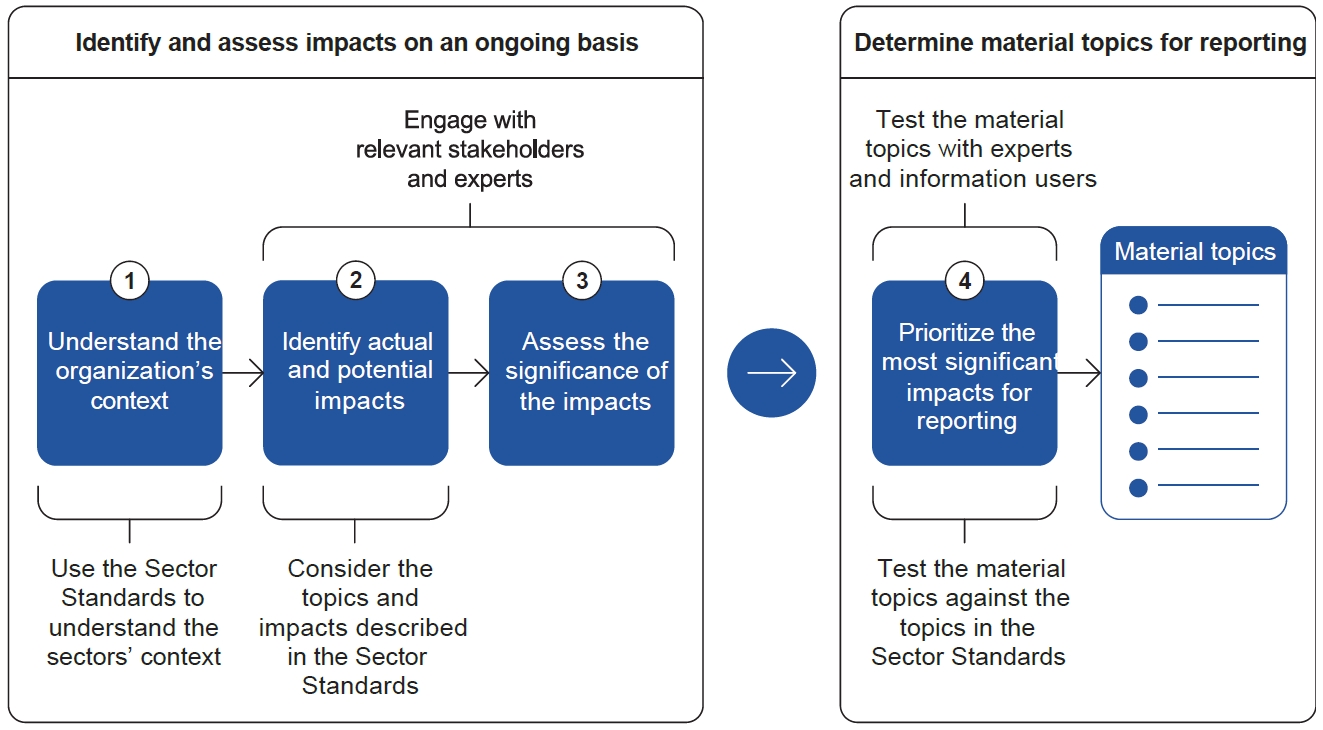

3. Identification of material topics and the setting of boundaries

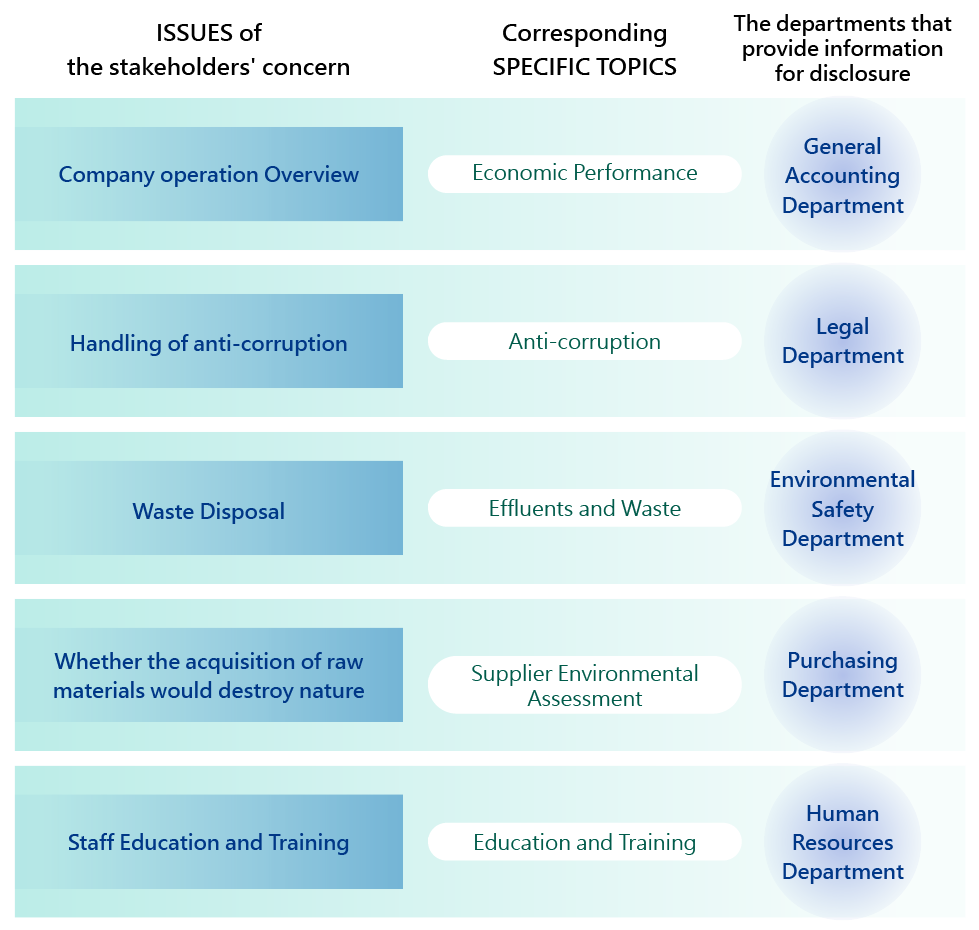

Material topics refer to the topics valued by stakeholders and can have high degree of impact on the corporate operation and development. Companies can identify material topics based on their impact on economy, environment and society to evaluate the appropriateness of the current strategies and goals of sustainable development promotion. They can also incorporate the performance indicators related to the material topics into the corporate performance management system to improve the communication efficiency of the report, enabling better credibility of the contents concerning organizational strategy and information, so as to reach the goal of continuous improvement and reaching the expectations of the stakeholders.

In GRI Standards, in addition to the complete identification of material topics and boundaries, they also reflect the organization's significant impact on economic, environmental and social aspects, and report on the organization's performance during the reporting period for the stakeholders to evaluate the organization. GRI Universal Standards 2021 considers various themes in sector standards and their impact, cross-references material topics with sector standards, and produces material topics in the report.

4. Selection of disclosure indicators

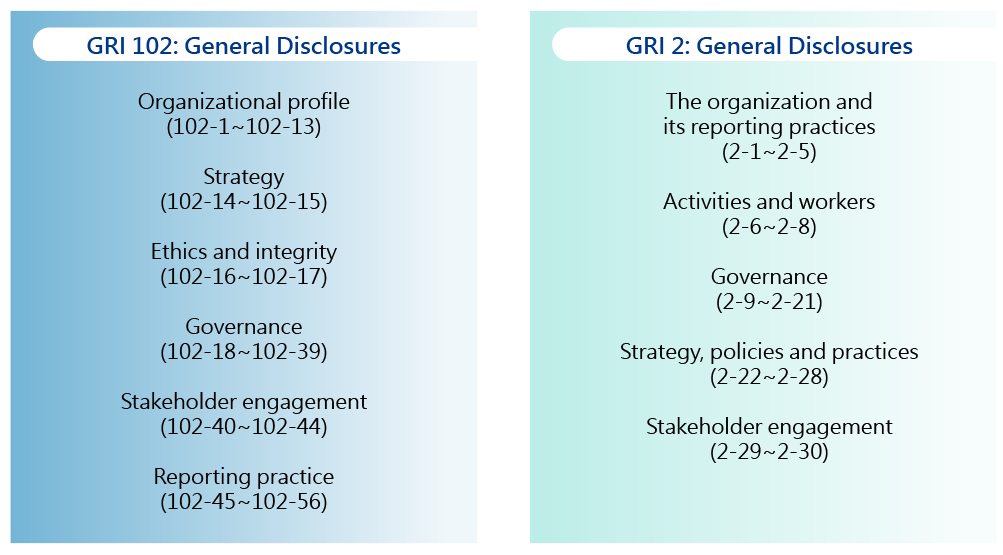

GRI 102:2016 provides two levels of disclosure for "core" or "comprehensive" "option-based" reports, which organizations can choose according to their own circumstances. In the future GRI General Standard 2021 will consolidate, fine-tune, and streamline the number of items in the general disclosure framework, and no longer distinguish between core and comprehensive options, and all items in GRI 2: General Disclosure must be disclosed when compiling reports in compliance with the GRI standard.

5. Data collection and content compilation

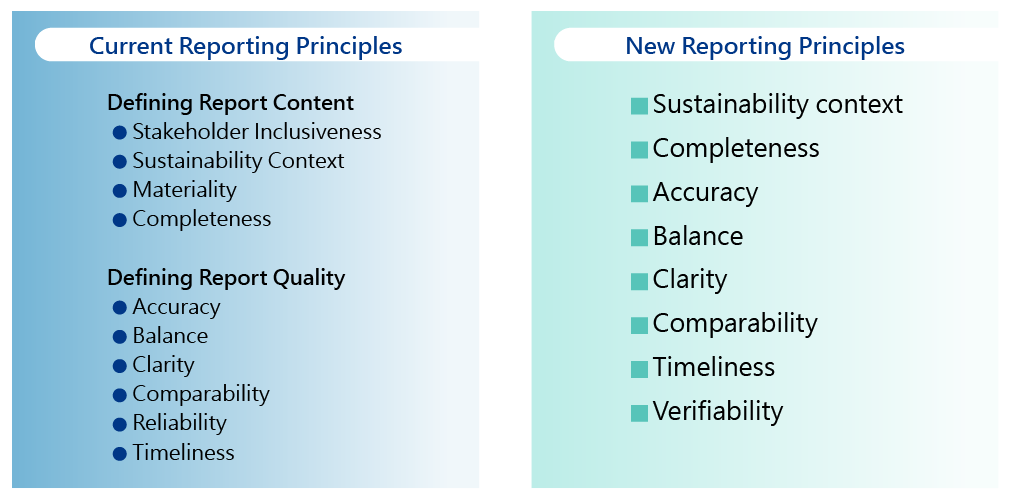

In addition to the disclosure in accordance with the GRI Standards, the sustainability report must also consider the reporting principles. The 4 reporting principles that defined the content of the report and the 6 reporting principles that defined the quality of the report were consolidated into 8 reporting principles in the new GRI Universal Standards 2021.

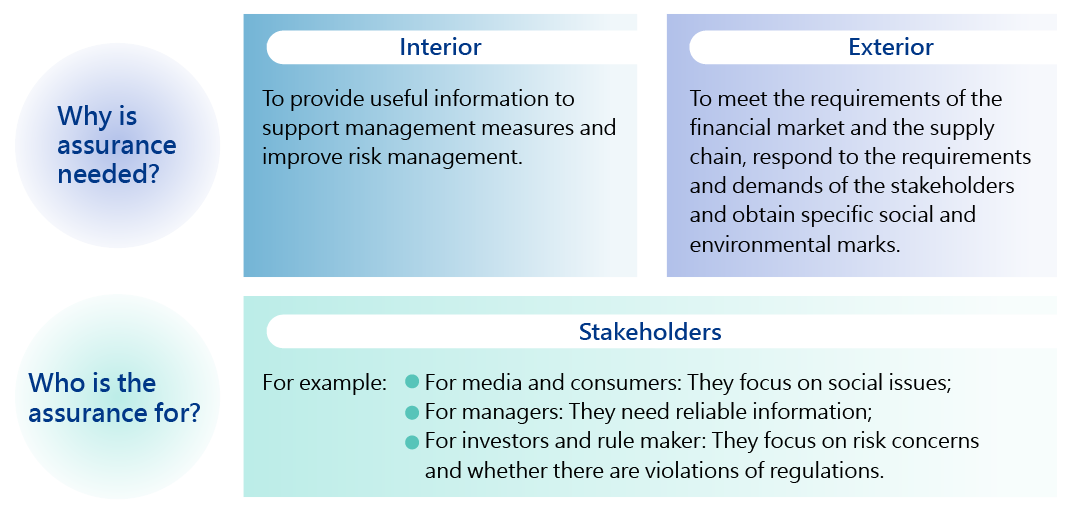

6. Internal and external verification of the report

The advantage of getting the verification from an impartial third party lies in the establishment of trust. A responsible company has to accurately communicate its strategies. Through the improvement of transparency of the report, the company shows its integrity and commitment to policy, impact and sustainable development to its stakeholders, which would be helpful in attracting investment and improving employee participation and customer confidence.

The British Standards Institution AccountAbility's AA1000 Assurance Standard (AA1000AS) was published in 2008, which is the only assurance standard that covers social responsibility and stakeholder participation and also the most commonly used standard for third-party verification of CSR Report among domestic companies. This standard requires assurance practitioners to evaluate the reporting party in accordance with the 4 principles of accountability, namely the inclusivity, materiality, responsiveness and impact, focusing on the perspectives of social responsibility and stakeholder participation to ensure the performance quality of the organization's corporate social responsibility report and related processes, systems as well as capabilities.